|

|

|

|

|

|

General Beata Gratton 1 Dec

|

|

|

|

|

|

General Beata Gratton 1 Dec

Justin Trudeau’s government, which has delivered the biggest COVID-19 fiscal response in the industrialized world, announced plans for another dose of stimulus and vowed to continue priming the pump as long as needed.

Finance Minister Chrystia Freeland unveiled $51.7 billion of new spending over two years in a mini-budget Monday, led by an enhanced wages subsidy for business. Freeland also pledged, without detailing, another $70 billion to $100 billion of additional stimulus over three years to spur the recovery.

But the finance minister clearly heeded calls for fiscal prudence. She put off any major structural spending announcements, promised any additional stimulus will be temporary and introduced new taxes on digital giants including Netflix, Amazon, and Airbnb, to help pay for it all.

“Our government will make carefully judged, targeted and meaningful investments to create jobs and boost growth,” Freeland said. It will provide “the fiscal support the Canadian economy needs to operate at its full capacity and to stop COVID-19 from doing long-term damage to our economic potential.”

Freeland revised higher the nation’s projected deficit this year to $381.6 billion, or 17.5% of GDP. That’s up from a deficit of 1.7% of GDP last year. According to estimates from the International Monetary Fund, no major economy will show a bigger fiscal swing in 2020.

The budgetary red ink is projected at $121 billion next year, before any additional stimulus. In total, spending linked to the government’s COVID response accounted for C$75 billion of this year’s deficit, and C$51 billion next year.

Based on Monday’s projections, the deficit is seen gradually narrowing to about $51 billion in two years and $25 billion by 2025.

The planned stimulus over the next three years will total no more than 4% of GDP, which the document said is in line with the Bank of Canada’s estimate of the level of slack in the economy. Freeland said, “fiscal guardrails” tied to the labour market would help determine the extent of the additional stimulus.

Among the measures announced today, Freeland boosted the government’s wage subsidy program (Canada Emergency Wage Subsidy, CEWS) to cover as much as 75% of payroll costs for businesses and extended its commercial rent subsidy and lockdown support top-ups until March. Both were slated to run out on December 20. The current cap on CEWS was 65%.

The federal government plans to create a new funding program to help restaurants, tourism companies and other businesses in industries hardest hit by COVID-19.

The Highly Affected Sectors Credit Availability Program (HASCAP), which was announced in the government’s fiscal update Monday, will offer eligible businesses loans of up to $1 million, with a 10-year term.

The money will be lent by banks or other financial institutions, but guaranteed by the federal government.

“We know that businesses in tourism, hospitality, travel, arts and culture have been particularly hard-hit. So we’re creating a new stream of support for those businesses that need it most — a credit availability program with 100-per-cent government-backed loan support and favourable terms for businesses that have lost revenue as people stay home to fight the spread of the virus,” Finance Minister Chrystia Freeland said in her prepared speech to the House of Commons.

Establishing a national childcare plan is a key long-term goal, with Freeland vowing a detailed plan in next year’s budget. In her forward to the fiscal update, she described the daycare strategy as “a feminist plan” that also “makes sound business sense.”

As a start, the Liberals are proposing in their fiscal update to spend $420 million in grants and bursaries to help provinces and territories train and retain qualified early childhood educators.

The Liberals are also proposing to spend $20 million over five years to build a child-care secretariat to guide federal policy work, plus $15 million in ongoing spending for a similar Indigenous-focused body.

The money is designed to lay the foundation for what will likely be a big-money promise in the coming budget.

Current federal spending on child care expires near the end of the decade, but the Liberals are proposing now to keep the money flowing, starting with $870 million a year in 2028.

There is also money for action on climate change. The government allocated C$2.6 billion in grants for homeowners to improve efficiency and $150 million over three years for electric vehicle charging stations.

The government also detailed some help for the hard-hit tourism sector, including funding for airports. But with Transport Minister Marc Garneau’s negotiations with airlines underway, there is no specific money for carriers including Air Canada and WestJet Airlines Ltd.

Bottom Line

There will continue to be great concern about the largest budget deficits since World War II. Does Canada really need the proportionately largest COVID fiscal response in the industrialized world? The outlook is somewhat less dire than when the government released a fiscal snapshot in July. The unemployment rate at 8.9% is down materially from May’s 13.7% high but well above February’s 5.6%. The economy recovered ground through the third quarter, although the second wave of pandemic and ensuing restrictions undoubtedly will topple economic activity this quarter.

There is little worry that the government can sustain a massive deficit this year. It can, given low debt levels entering the crisis and historically low interest rates. But now that it has no fiscal guardrails, there’s a risk debt-to-GDP will continue to rise in the medium term if it continues to spend ambitiously.

The government is adding a new revenue source by taxing large digital companies. Still, in time, with this level of spending, they will be tempted to raise taxes on domestic sources, for example, hikes in the GST and higher capital gains taxes. This would be misguided, given the fragility of the recovery.

There is a greater risk that the government is overdoing the stimulus with vaccines on the horizon than undergoing it. Canada’s programs have been generous and household-focused compared to our G7 peers. The government must be strategic in assuring that new program spending is focused on future growth, beyond the pandemic, so that our debt-to-GDP will resume its downward trend. The risk is that once created; it is difficult to rein in spending.

General Beata Gratton 18 Nov

The average home price in Canada continued to trend higher in October as housing supply fell to a fresh record low.

The Canadian Real Estate Association reported the average sale price at $607,250 for the month, an increase of 15.2% from a year earlier.Removing the high-priced markets of Toronto and Vancouver, the national average price was $480,250, up 19.5% from a year ago.

Sales, meanwhile, were up 32.1% year-over-year and set a new record for September by a margin of 14,000 transactions, according to CREA.This marks the fourth-straight month that activity has been up in nearly all Canadian markets.

“For anyone waiting for the Canadian existing home market to begin to settle down following this summer’s surprisingly strong recovery, they’re going to have to wait a little longer,” said Shaun Cathcart, CREA’s senior economist.

“Many reasons have been suggested for why this is when many traditional drivers of the market, economic growth, employment and confidence in particular, are currently so weak,” he continued. “Something worth considering is how many households are choosing to pull up stakes and move as a result of COVID-19 and all the associated changes to our lives.

Yet, housing inventory ticked down to just 2.5 months, a fresh record low. This is how long it would take to liquidate current inventories at the current sales rate. And CREA noted that 18 Ontario markets were under one month of inventory by the end of October.

That, of course, has kept upward pressure on home prices across the country.  Here’s a look at how some regional and local housing markets performed in October:

Here’s a look at how some regional and local housing markets performed in October:

Analysts were in agreement that limited housing supply is the key factor keeping the country’s housing market going and going like the Energizer bunny.

“Sellers were in the driver’s seat in virtually all major markets, holding commanding sway over prices in Central Canada and most of the Atlantic region,” noted RBC economist Robert Hogue. “The main exceptions were in downtown condo segments of some of Canada’s largest cities where supply has soared.”

BMO senior economist Robert Kavcic agreed, writing, “very limited supply in areas that are seeing an influx of demand is boosting prices, with the pace across many markets ranging from solid to historic…As it turns out, 2020 will be a banner year for the Canadian housing market.”

But there are other factors at play as well.

“Clearly exceptionally low interest rates are keeping the market’s wheels well-greased at this stage. They make it easier for many first-time homebuyers and move-up buyers to jump into the market,” Hogue said. “Yet work-from-home is possibly an even more powerful driver of activity. The pandemic altered work arrangements for millions of Canadians—potentially permanently for many of them—prompting a large-scale re-evaluation of housing needs.”

General Beata Gratton 18 Nov

Today’s release of October housing data by the Canadian Real Estate Association (CREA) shows national home sales fell 0.7% month-over-month (m-o-m) from September’s record high (see chart below). This is the first decline in five months, as market conditions remained tight and prices continued to rise. Competition remains intense in the detached-home market and townhouses, but condo apartment sales have slowed as new listings surge, especially in the Greater Toronto Area (GTA).

The small change from September to October reflected gains in about half of all local markets offset by declines in the other half. Among the larger markets, activity was up in Montreal, the Fraser Valley, Calgary and Edmonton. By contrast, sales fell back in the GTA, Hamilton-Burlington, Ottawa and Greater Vancouver.

Actual (not seasonally adjusted) sales activity posted a 32.1% y-o-y gain in October. It was a new record for that month by a margin of more than 14,000 transactions. For the fourth straight month, sales activity was up in almost all Canadian housing markets compared to the same month in 2019. Among the few markets that were down on a year-over-year basis, it is possible for the handful that is in Ontario simply do not have the supply at the moment.

This year, some 461,818 homes have traded hands over Canadian MLS® Systems, up 8.6% from the first 10 months of 2019. In fact, it was the second-highest January-October sales figure on record, trailing only 2016. It is possible that 2020 could prove itself to be a record year for housing activity–certainly in opposition to what many thought when the pandemic hit in March. There is no doubt that COVID-19 has caused many households to uproot and change homes based on their altered lifestyle and working situation. Much of this activity would not have happened had the pandemic not struck.

New Listings

The number of newly listed homes climbed 2.9% in October. The overall gain in new supply in October was driven by more new listings in the GTA, B.C.’s Lower Mainland and Ottawa. As with sales activity, actual (not seasonally adjusted), new listings set a new record for October; however, it was by far less of a margin than sales. Meaning market conditions are still very tight in many parts of the country.

The Toronto Real Estate Board reported that the pace of annual sales growth far outstripped growth in new listings in the detached market segment. Conversely, the condominium apartment market segment experienced more than double the new listings than in October 2019, whereas sales were only up by 2.2% over the same period (see chart below).

“Competition between buyers of single-family homes, and particularly detached houses, remained strong last month and continued to support double-digit annual rates of price growth in many GTA neighbourhoods. In contrast, condo buyers have benefitted from much more choice compared to last year. Pre-COVID polling had already pointed to an increase in investor selling in 2020. The pandemic only added to this trend with a stall in economic growth and a halt to tourism impacting cashflows for many investors,” said Lisa Patel, TRREB’s President.

The dearth of tourists has devastated the short-term rental condo market, many of which are listed on Airbnb. And a dramatic decline in immigration hurt the long-term condo rental space. Rents overall have fallen in the GTA, and many investors are trying to sell. As well, many buyers of yet-to-be-delivered new condos are trying to flip their contracts. The federal government initiatives to increase immigration in 2021, if successful, will help remediate this situation. Still, tourism will not open back up until a vaccine is widely distributed around the world. There has been some good news on that front.

With new supply up in October and sales relatively little changed, the national sales-to-new listings ratio eased to 74.3% – still among the highest levels on record for the measure. The long-term average for the national sales-to-new listings ratio is 54.1%.

Based on a comparison of sales-to-new listings ratio with long-term averages, about a third of all local markets were in balanced market territory in October, measured as being within one standard deviation of their long-term average. The other two-thirds of markets were above long-term norms, in many cases well above.

There were just 2.5 months of inventory on a national basis at the end of October 2020 – the lowest reading on record for this measure. At the local market level, some 18 Ontario markets were under one month of inventory at the end of October.

The Aggregate Composite MLS® Home Price Index (MLS® HPI) rose by 1% m-o-m in October 2020. Of the 39 markets now tracked by the index, all but one were up between September and October (see table 1 below).

The non-seasonally adjusted Aggregate Composite MLS® HPI was up 10.9% on a y-o-y basis in October – the biggest gain since July 2017.

The largest y-o-y gains – more than 25% – were recorded in Ontario’s Quinte & District and Woodstock-Ingersoll.

Y-o-y price increases in the 20-25% range were seen in Ottawa, London & St. Thomas, Tillsonburg District and some Ontario cottage country areas.

Y-o-y price gains followed this in the range of 15-20% in Barrie, Hamilton, Niagara, Guelph, Bancroft and Area, Brantford, Cambridge, Huron Perth, Kitchener-Waterloo, North Bay, Peterborough and the Kawarthas, Simcoe & District, Montreal and Greater Moncton.

Prices were up in the 10-15% range compared to last October in the GTA, Oakville-Milton, Mississauga and Northumberland Hills.

Meanwhile, y-o-y price gains were in the 5-10% range in Greater Vancouver, the Fraser Valley, the Okanagan Valley, Regina, Saskatoon, Winnipeg and Quebec City. Gains were less than 4% in Victoria and elsewhere on Vancouver Island, as well as in St. John’s, and prices were just inside positive territory y-o-y in Calgary and Edmonton.

The actual (not seasonally adjusted) national average home price set another record in October 2020, coming in at $607,250. This was up 15.2% from the same month last year.

Bottom Line

Housing strength is largely attributable to record-low mortgage rates and pent-up demand by households that have maintained their income level during the pandemic. The hardest-hit households are low-wage earners in the accommodation, food services, and travel sectors. These are the folks that can least afford it and typically are not homeowners. The good news is that the housing market is contributing to the recovery in economic activity.

Since Pfizer’s announcement that they have a highly effective vaccine in the works, interest rates in the US have edged upward. This has been mitigated in part by the dramatic surge in COVID cases worldwide and tighter restrictions on activity. This morning, Modernal Inc. said its COVID-19 vaccine was 94.5% effective in preliminary analysis of a large late-stage clinical trial, another sign that a fast-paced hunt by scientists and pharmaceutical companies is paying off with potent new tools that could help control a worsening pandemic. This great news has pushed up the US and Canadian bond yields, leading many to suggest that a rise in mortgage rates can’t be far behind. Stock markets are rising sharply, especially in the US, where they are hitting new record highs.

The 5-year Government of Canada bond yield is currently at .45%. It had been as low as .39% recently and .28% over the past year. The good news on the vaccine front may well be overblown given that expanded pandemic restrictions and record cases will dampen economic activity well through the winter months, mitigating the upward pressure on rates. Any mortgage rate increases will be 10 basis points or less, although discounts might start to disappear.

General Beata Gratton 6 Nov

The October Labour Force Survey, released this morning by Stats Canada, showed an employment increase of 83,600–well below the 378,000 gain in September and average monthly gains of 395,000 over the past six months (see chart below). Several provinces tightened public health restrictions last month in response to a spike in COVID-19 cases. These measures were targeted at indoor restaurants and bars, and gyms.

Most of the job gains last month were in full-time work. Among those who worked at least half their usual hours, the number working from home increased by 150,000. Working remotely continues to be an important adaptation to COVID-19 health risks, with 2.4 million Canadians who do not normally work from home doing so in October.

The unemployment rate was little changed at 8.9% in October but remained well-below the May peak of 13.7%. In addition to the unemployed, 540,000 Canadians wanted to work in October but did not search for a job, down 39,000 from September and continuing a downward trend from a peak of 1.5 million in April. If people in this group were included as unemployed, the adjusted unemployment rate in October would be 11.3%.

Long-term joblessness—defined as unemployed and looking for work or temporary layoff for 27 weeks or more— increased again in October. Not surprisingly, more than half (53.3%) of the long-term unemployed were living in a household reporting difficulty meeting necessary expenses. As of October, the long-term unemployed totalled 448,000, or one-quarter of all unemployed people. September and October increases in long-term unemployment are by far the sharpest recorded since comparable data became available in 1976.

Job Gains Slow in Central Canada

Employment increased in the wholesale and retail trade industries in Ontario, two sectors largely unaffected by new COVID-19 restrictions. After five months of gains totalling 154,000, employment in Ontario’s accommodation and food services was virtually unchanged in the month and remained 15.7% below its pre-COVID February level. Employment declined in transportation and warehousing.

Following five consecutive months of gains, employment was little changed in Quebec in October, and the unemployment rate edged up 0.3 percentage points to 7.7%. Employment gains spread across several services-producing industries were partly offset by a drop of 42,000 in the accommodation and food services industry. The public health alert level in Montréal and Québec City was raised to “red” on October 1, which led to the closure of indoor restaurants and many cultural facilities. Travel between regions in the province was also discouraged. Over the subsequent two weeks, several other Quebec regions went to red alert, and additional measures were introduced.

Employment Grows in Alberta and BC

In British Columbia, employment grew by 34,000 (+1.4%) in October, adding to gains over the previous five months (+302,000). The unemployment rate fell for the fifth consecutive month, down 0.4 percentage points to 8.0% in October. In Vancouver, employment increased by 52,000 (+3.8%) and was within 4.3% of its pre-COVID level.

In Alberta, employment rose by 23,000 (+1.1%), the fifth increase in six months. Following large employment losses earlier this year, Calgary has posted four consecutive employment gains since summer, totalling 101,000 (+13.6%). Recent employment increases in Edmonton have been more modest, up 60,000 (+9.0%) since summer.

October employment gains in Alberta were spread across several industries, including healthcare and social assistance, transportation and warehousing, and wholesale and retail trade. Employment in natural resources edged up in the month but was down 5.2% on a year-over-year basis.

In Newfoundland and Labrador, employment grew (+5,900) in October, while the unemployment rate fell 2.0 percentage points to 12.8%. Employment was also up in Prince Edward Island (+900), while the unemployment rate was virtually unchanged at 10.0%.

Hard-Hit Sectors of the Economy

The accommodation and food services industry was most directly affected by the recent tightening of public health measures—and, for the first time since April, employment declined in this industry in October. Employment in the arts, entertainment, and recreation sectors was farther from pre-COVID levels than any other sector in August. The next few months will shed light on the impact of public health restrictions on employment in this sector, which, like the accommodation and food services industry, has strong ties to travel and tourism.

With restrictions on travel and gathering still in place, the continuing impact of COVID-19 has been much more significant for the transportation of people than of goods. For example, the August Survey of Employment, Payrolls and Hours found that payroll employment in transit and ground passenger transportation was down by 17.8% from February to August, while payroll employment in truck transportation—primarily for goods—was down 7.9% for the same period. Similarly, in August, major Canadian airlines carried 86.8% fewer passengers than 12 months earlier, and Canadian railways carried 14.7% less freight.

In construction, employment was little changed for the third consecutive month in October, following increases totalling 190,000 (+16.2%) from April to July. Employment in construction was 7.5% (-112,000) below its February level in October. Recent data on housing starts showed a decline of 5.0% from September 2019 to September 2020, following two months of strong year-over-year increases.

Employment Growth Resumed in Retail Trade

Following a pause in September, employment growth resumed in retail trade, rising by 31,000 (+1.4%) in October, with most of the increase in Ontario. From February to April, employment declined by over one-fifth (-22.9%; -517,000) due to retail businesses’ closures during the first wave of COVID-19. In October, public health measures associated with the second wave did not include retail businesses’ requirements to close. Employment in this industry was 5.1% (-115,000) below its pre-COVID level and down by 2.4% (-54,000) compared with October 2019.

The Winners

Employment exceeded pre-COVID levels in three industries in October—wholesale trade; professional, scientific and technical services; and educational services.

In wholesale trade, employment increased by 15,000 (+2.3%) in October, driven by Alberta increases. Employment in this industry was 5.6% (+35,000) above its February level. The wholesale trade release’s latest results show that sales increased for the fourth consecutive month in August and were 1.7% above pre-COVID-19 levels.

Employment rose for the fourth consecutive month in professional, scientific and technical services, up 42,000 (+2.7%) in October and led by Ontario (+23,000). With this gain, this industry’s employment was 3.3% (+51,000) higher than its pre-COVID level. Job security among employees in this industry includes computer systems design and related services; architecture, engineering and related services; and legal services tend to be higher than in other industries.

Employment was little changed in educational services in October but exceeded its February level by 2.8% (+39,000). Compared with October 2019, employment in this industry increased by 32,000, in part a reflection of some jurisdictions increasing staffing levels to support classroom adaptations brought on by COVID-19.

Compared with other industries, a relatively high share of workers in educational services (25.8% in 2019) is temporary employees, reflecting the relatively high prevalence of teaching staff hired on a contract basis. While the number of temporary employees decreased markedly following the initial COVID-19 economic shutdown, it had rebounded in October (little changed on a year-over-year basis, not seasonally adjusted), helping to boost overall employment in the industry. Permanent employees in educational services also contributed to the recovery of this industry on a year-over-year basis. In October, the number of permanent employees was up 5.6% compared with 12 months earlier (not seasonally adjusted).

Bottom Line

The economic recovery remains dependent on the evolution of the pandemic. It is likely that extensive lockdown measures, such as the widespread closures imposed early in the pandemic, will not be reintroduced. However, more localized and moderate containment measures will ebb and flow. The Bank of Canada suggests that vaccines and effective treatments will be widely available by mid-2022, at which time the direct effects of the pandemic on economic activity will have ended. However, households’ precautionary behaviour and the effects of the uncertainty surrounding COVID-19 are likely to linger.

The pandemic is also likely to have persistent effects on the preferences and behaviours of consumers and businesses. This could lead to lasting changes to the economy’s structure and could weigh on its potential output. The sizes and timing of such effects are difficult to estimate precisely. Given these considerations, the outlook for Canadian and global economic activity remains unusually uncertain.

The most recent COVID Consumer Spending Tracker, produced by the RBC economics group, that second wave worries have shifted more spending online. Household, clothing, and retail spending held steady, while travel spending continued to decline. Spending on dining out edged downward last month as cooler whether rendered outdoor dining less appealing. Entertainment expenditures ticked downward as well.

The regional real estate boards in Vancouver, Toronto and Montreal recently released their October housing reports showing continued sales activity and upward price prices except in the condo space, particularly smaller condos that were bought on spec for the rental market. With the nosedive in tourism, the short-term rental market has collapsed. Many of these former Airbnb properties are either for sale or have moved into the long-term rental space, driving down prices. The dearth of immigration this year has also exacerbated the decline in rent. Condo listings are rising faster than sales in many regions. In contrast, lower rise properties remain in very tight supply, and prices continue to rise. We will provide more details on housing trends with the release of the CREA data late next week.

General Beata Gratton 6 Nov

The postponed spring housing market has now extended its run well into the fall, with home sales in Toronto and Vancouver up 25% and 29%, respectfully, compared to a year ago.

The high demand is continuing to put pressure on prices as well. The average selling price for all home types in Toronto rose 13.7% to $968,318, according to the Toronto Regional Real Estate Board (TRREB). However, there was a divergence between market segments, with detached home prices rising 14.8% to $1.204 million, while average condo prices were up just 0.7% to $622,122.

In Vancouver, the MLS Home Price Index composite benchmark price for all property types rose 6% to $1.045 million, according to the Real Estate Board of Greater Vancouver (REBGV).

It was a similar story in Greater Montreal, where sales and prices were also up sharply in October. The Quebec Professional Association of Real Estate Brokers (QPAREB) reported that Montreal saw a 37% jump in sales, while home prices were up 21% for single-family homes and 16% for condos.

“Home has been a focus for residents during the pandemic. With more days and evenings spent at home this year, people are re-thinking their housing situation,” REBGV chair Colette Gerber said in a release.

But there’s another factor at play that’s helping to keep housing relatively affordable despite the recent run-up in prices.

“Extremely low interest rates have also made homeownership more accessible for first-time buyers and altered the calculations for potential move-up buyers,” Mortgage Professionals Canada chief economist Will Dunning noted in his latest consumer report. “For people in reasonably stable economic situations who expect that stability to continue (and the survey data indicates that most of us are in this situation), there is currently heightened interest in home buying.”

With today’s fixed mortgage rates at record lows and available for about the same as a variable rate, or even less, it’s no wonder more homebuyers are again flocking to fixeds.

A recent BMO survey confirmed this, finding that 57% of homebuyers said they would opt for a fixed mortgage rate when it comes time to secure a mortgage. Of those on the fence, another 30% said the pandemic has made them more likely to gravitate towards a fixed rate.

Just 8% of respondents said they would choose a variable rate.

The survey also found…

Genworth MI Canada, now officially operating as Sagen MI Canada, has entered into an agreement with U.S.-based Brookfield Business Partners L.P.

Under the deal, Brookfield, which already owns 57% of Genworth’s common shares, will purchase the outstanding shares at a price of $43.50 each, a 22% premium on the company’s closing share price on October 23.

The deal was approved unanimously by the company’s board of directors, except for one director who was recused due to a conflict of interest.

“The Transaction, together with our Company’s recent rebranding as Sagen MI Canada, represents an exciting new chapter for the Company,” Stuart Levings, President and CEO, said in a release. “We look forward under Brookfield’s ownership to continuing to work with lenders, regulators and mortgage professionals to help people responsibly achieve and maintain the dream of home ownership.”

General Beata Gratton 2 Nov

Mortgage shoppers take note: Cheap money is here to stay, at least for the next two years, the Bank of Canada reaffirmed during its interest rate decision on Wednesday.

The BoC had previously provided guidance that rates would remain at their effective lower bound—currently 0.25%—“until 2 percent inflation target is sustainably achieved,” but went a step further this time by providing a specific year.

“The Governing Council will hold the policy interest rate at the effective lower bound until economic slack is absorbed…In our current projection, this does not happen until into 2023,” the Bank’s statement read.

As part of the announcement, the BoC decided to leave its current policy rate at 0.25%, where it’s been since March.

While the Bank left its policy rate untouched, it did announce changes to its Quantitative Easing program, whereby the BoC has been purchasing bonds to maintain market liquidity, which has helped keep mortgage rates low.

That bond-buying will be reduced to $4 billion per week from the current $5 billion, and purchases will increasingly shift to longer-term bonds.

“Our main message today is that it will take quite some time for the economy to fully recover from the Covid-19 pandemic,” BoC Governor Tiff Macklem said during a press conference that followed the rate announcement. “The Bank of Canada will keep providing monetary stimulus to support the economy through the recovery.”

And that recovery is facing fresh headwinds as a result of a second wave of the pandemic, which is intensifying by the week.

Despite a stronger-than-expected rebound in unemployment and GDP over the summer, the Bank said “growth is expected to slow markedly.” Looking ahead to 2021 and 2022, the Bank expects the economy to grow by 4% on average each year.

“After a tumultuous spell for all forecasters, the Bank’s view on the economy has largely moved into line with consensus,” BMO Economics Chief Economist Douglas Porter wrote in a research note. “And the main message there is that growth will be put on hold in Q4 by the second wave, but it won’t go into reverse, and should resume in 2021.”

The Bank’s announcement affects both fixed and variable rates. Fixed rates are expected to remain low, and likely fall further, due to the Bank’s renewed commitment to purchasing longer-term bonds, which will help keep rates low for the ever popular 5-year fixed term.

The Bank’s announcement affects both fixed and variable rates. Fixed rates are expected to remain low, and likely fall further, due to the Bank’s renewed commitment to purchasing longer-term bonds, which will help keep rates low for the ever popular 5-year fixed term.

And the Bank’s guidance on maintaining its overnight rate at 0.25% until at least 2023 bodes well for existing variable-rate holders, to the extent they can rest assured their rates won’t rise.

But the Bank’s continued reluctance to entertain negative rates also means that new floating-rate mortgage holders aren’t likely to see their rates fall any further. (Although, an additional rate cut can’t be completely ruled out. Overnight Index Swaps markets are still pricing in a 15% chance of a 25-bps cut in the next 12 months.)

In this environment, many borrowers are gravitating towards fixed rates.

A recent BMO survey found that 57% of first-time buyers said they’ll choose a fixed rate when they’re ready to secure their mortgage. Another 30% who were undecided said COVID has made them more likely to choose a fixed rate.

“The best nationally available 5-year fixed and variable rates are currently just 5 bps apart. Insured 5-year fixed rates are below variable rates,” wrote RateSpy founder Rob McLister. “Most consider a 5 bps rate premium peanuts for peace of mind, as they should…Even if the BoC dropped rates 25 bps, the cost of being wrong by choosing a 5-year fixed is modest ($245 of extra interest per year per $100,000 of mortgage).”

And while the Bank said rate hikes are off the table until at least 2023, some economists believe they’ll remain where they are for longer than that.

“We see this as a reasonable timeline but wouldn’t be surprised if the overnight rate remained at 0.25% into 2024 as well,” economists at National Bank of Canada wrote. “As always, the progression of the pandemic will be in the driver’s seat here and ultimately dictate the health of the economy, and thus, monetary policy.”

General Beata Gratton 28 Oct

As expected, the Bank held its target overnight rate at the effective lower bound of 25 basis points with the clear notion that negative policy rates are not in the cards. Instead, the central bank will continue to rely on large-scale asset purchases–quantitative easing (QE). The central bank is recalibrating its QE program as promised in recent weeks. In mid-October, it announced that it would end its Repo, Bankers Acceptance and Canada Mortgage Bond purchases this month, as they are no longer needed to assure liquidity in those markets. The volumes of purchases have declined sharply since April. This move will have minimal impact on market interest rates.

The Governing Council announced today it would also gradually reduce purchases of federal government bonds from at least $5 billion to at least $4 billion per week. “The Governing Council judges that, with these combined adjustments, the QE program is providing at least as much monetary stimulus as before.”

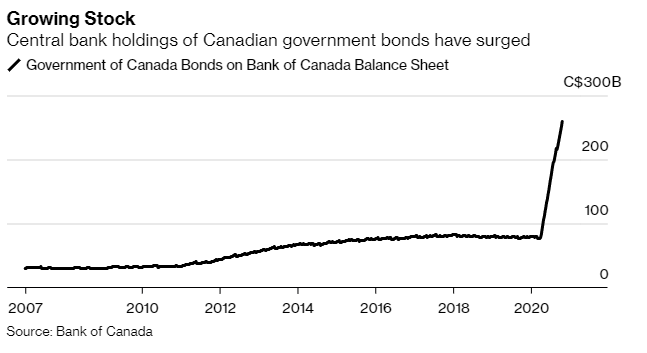

The PC opposition party has been warning Governor Macklem of the risks of financing Trudeau’s government spending. But the Bank has little alternative but to step-up its buying of newly issued benchmark bonds–those currently being sold by the government, as opposed to older debt that is becoming increasingly illiquid. As reported in Bloomberg News, “It means the bank’s quantitative easing program will increasingly mirror government debt sales at a time when opposition lawmakers are warning it against directly financing Prime Minister Justin Trudeau’s fiscal agenda.” (See chart below). The Bank already owns more than a third of all outstanding Government of Canada debt, proportionately more than most central banks because Canada ran budget surpluses, which paid down debt for so long.

Virtually every major central bank in the world is conducting an emergency QE program in response to the COVID-19 crisis. The Bank of Canada says its QE program reinforces its commitment to hold interest rates at historic lows over the next few years until the annual inflation rate is sustainably at its target 2% level. Today’s October Monetary Policy Report indicates they will likely keep the overnight rate at 0.25% until 2023.

The central bank has no intention of paring back stimulus, with risks to the economy growing amid the second wave of COVID-19 cases. “As the economy recuperates, it will continue to require extraordinary monetary policy support,” the bank said. “We are committed to providing the monetary policy stimulus needed to support the recovery and achieve the inflation objective.”

October Monetary Policy Report

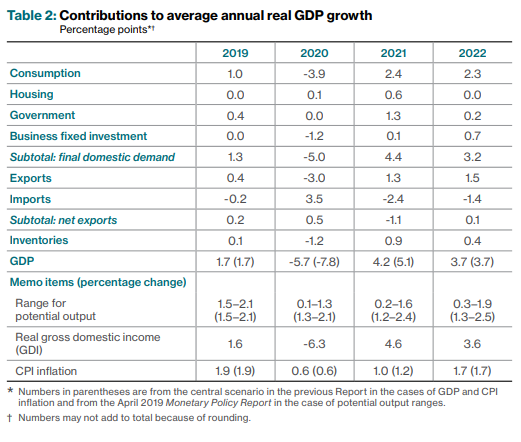

The Bank of Canada’s forecast for Canadian growth is shown in the table below. The economic recovery is projected to be prolonged, underpinned by policy support but largely influenced by the evolution of the virus, ongoing uncertainty and structural changes to the economy. These changes could result in longer-term shifts of workers and capital across different regions and sectors of the economy. This adjustment process weighs on the Bank’s estimates of potential growth.

After declining by about 5 1/2 percent in 2020, the economy is expected to expand by almost 4 percent on average in 2021 and 2022. Two factors will likely lead to quarterly patterns of growth that are unusually choppy: localized outbreaks and containment measures and varied recovery rates across industries.

Inflation is expected to remain below the lower end of the Bank’s inflation-control target range of 1 to 3 percent until early 2021, largely due to the effects of low energy prices. Subsequently, inflation is anticipated to be within the target range, but economic slack will continue to put downward pressure on inflation throughout the projection period.

The Reopening Phase Was Strong But Uneven

Growth is estimated to have rebounded strongly in the third quarter, reversing about two-thirds of the decline observed in the first half of the year. A sizable bounce back in activity resulted from a rebound in foreign demand, the release of pent-up demand for housing and some durable goods, and robust policy support.

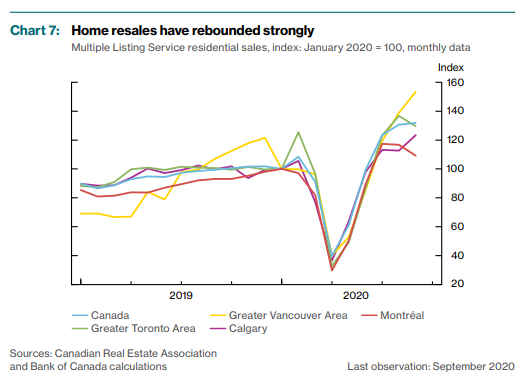

Housing activity recovered sharply in the third quarter, supported by historically low financing costs, resilient incomes for higher-earning households, and extra sales and construction that made up for delayed spring activity (Chart 7). By September, cumulative resales are estimated to have compensated for the missed activity during the normally busy spring market. Housing activity may also be benefiting from changes in preferences. In particular, more than one-quarter of respondents to the Canadian Survey of Consumer Expectations in the third quarter of 2020 reported they would like to move to a larger or single-family home because of the pandemic. The strength of the housing market recovery, combined with a tight resale market, has led to the rapid growth of house prices in some markets. In contrast to the appreciation of house values observed in Toronto and Vancouver in 2016, price growth has been strongest in markets with moderate loan-to-income ratios, such as Ottawa, Montréal and Halifax.

Bottom Line

Interest rates will remain low for the foreseeable future. The pandemic will largely determine the growth of the economy and the government’s response. Experts suggest that this second wave will last for much of the winter and that a widely dispersed vaccine will not be available until at least well into 2021. As tough as that is to take, Canada is still doing a better job of containing the virus than the US, UK and the Euro area. Output is likely to remain below pre-pandemic levels everywhere through the end of 2022, the Bank of Canada’s forecast horizon.

General Beata Gratton 26 Oct

This Wednesday, the Bank of Canada will release its interest rate announcement and the October Monetary Policy Report. Most people expect the overnight rate to remain at 0.25%, where it has been since the pandemic hit. A few have suggested that the Bank could take a page from Australia and reduce overnight rates by 15 basis points. I don’t think so.

Canada’s economy is not as similar to Australia’s as you might think. Yes, both countries speak mostly English, are commodity exporters, and have a currency called the dollar. But that is where the similarities end. Australia is largely a supplier to China and East Asia, while the US dominates Canada’s exports. And our major resource is oil rather than metals. Most importantly, the Bank of Canada believes that lower rates would not be helpful, given the squeeze they put on the banking system’s workings.

The Bank has committed to staying at 0.25% until economic conditions would be consistent with a sustained 2% inflation rate. With the second wave of COVID cases and rolling shutdowns upon us, the economic rebound will slow in the coming quarters. Moreover, it is unlikely we will see inflation averaging above 2% or higher through 2022. The base case forecast for overnight rates by the Bank of Canada will remain at 0.25% until 2023 unless we see a miraculous end to the pandemic far sooner than most experts predict.

Where the Bank will make policy changes is in quantitative easing–the buying of financial assets to improve liquidity in financial markets. The Bank’s Governing Council has, for months, hinted at the need for the current structure of the QE program to be “calibrated.” While there have been few details on what this means, we interpret it to imply a move away from a QE program supporting ‘market-functioning’ to one that attempts to achieve a ‘monetary policy objective.’ To some degree, this has already started.

On October 15, the Bank announced it would retire the Repo purchase program, the Bankers’ Acceptance purchase Facility and the Canadian Mortgage Bond Purchase Program (CMBP). These areas of the Canadian fixed income market are fully functioning at present, and the Bank likely felt ongoing support was no longer necessary. The end of the CMBP got the attention of some mortgage market participants who argued it spelled the end of declining mortgage rates. I think this is a misinterpretation of the Bank’s actions.

As the chart below shows, the use of the CMBP has waned considerably since its introduction in March. It just isn’t needed any longer to assure liquidity in the CMB market. Since August, lenders have only been using about $70 to $190 million per week of the BoC’s $500 million capacity. The last time lenders fully utilized, it was in April when the emergency program was clearly needed. Ending this program should have little impact on mortgage rates.

“As overall financial market conditions continue to improve in Canada, usage in several of the Bank of Canada’s programs that support the functioning of key financial markets has declined significantly,” the Bank said in announcing the changes. The program, designed to provide much-needed liquidity to the banking system to keep credit flowing during the worst of the crisis, has “fallen into disuse as the stresses from the pandemic eased, and markets became much more self-sufficient.”

The move follows the bank’s decision a month ago to reduce its purchases of federal government treasury bills and similar short-term provincial money market debt, citing improvements in the health of short-term funding markets.

The CMB purchase program is also dwarfed by the Bank’s Government Bond Purchase Program (GBPP), as the chart below shows. “The central bank has pledged repeatedly that it will maintain the highest-profile of its emergency asset-buying programs – its minimum $5-billion-a-week purchases of Government of Canada bonds – until the [economic] recovery is well underway. It has also so far maintained its two programs to purchase provincial and corporate bonds, even though both programs’ demand has been far below original expectations.

Mortgage rates in Canada have an 85% correlation with the 5-year Government of Canada bond yield, which has fallen sharply over the course of the pandemic crisis.

Bottom LineOf the three programs being wound down in the bank’s latest announcement, the biggest is the expanded term repo program, under which the central bank has purchased more than $200-billion of the short-term bank financing instruments since mid-March. The program hasn’t generated any purchases since mid-September.

The Bankers’ Acceptance Purchase Facility, involving short-term credit instruments typically used in international trade financing, was used heavily when introduced in March. Still, it hasn’t been tapped at all since late April. The central bank made about $47-billion in purchases under the program. However, all of those purchased assets have since reached maturity, meaning the central bank is no longer holding any bankers’ acceptances on its balance sheet.

The Canada Mortgage Bond Purchase Program predates the pandemic, but the Bank of Canada ramped up its purchases dramatically during the crisis. Since mid-March, it has accumulated about $8-billion of the bonds under its emergency measures through twice-weekly purchases directly from Canada Mortgage and Housing Corp. The size of the bank’s typical purchases in the past couple of months has been less than a quarter of what it was routinely buying in the spring.

These changes in the QE program will have little impact on interest rates and mortgage markets.

General Beata Gratton 26 Oct

Dominion Lending Centres continued its growth trajectory this month with several new announcements.

Earlier this month, Founders Advantage—which bought a controlling share of DLC in 2016—announced it has entered into an agreement to acquire 100% of DLC as part of a larger restructuring that will see DLC and Founders merge to create a new entity known as Dominion Lending Centres Inc. If approved, the new public company would trade under the symbol DLCG.

As part of the proposed deal, Dominion Lending Centres co-founder Gary Mauris will assume the role of Chief Executive Officer and Executive Chairman, while co-founder Chris Kayat will become Executive Vice-Chairman.

Recapping the company’s journey in a call with investors, Mauris touched on the initial reason for selling 60% of the company to Founders Advantage, saying at that point they were looking to de-risk somewhat, feeling it was the “prudent and responsible” thing to do.

Recapping the company’s journey in a call with investors, Mauris touched on the initial reason for selling 60% of the company to Founders Advantage, saying at that point they were looking to de-risk somewhat, feeling it was the “prudent and responsible” thing to do.

But Mauris added there were frustrations along the way after the sale, despite believing that the management team at FA had “very, very good intentions.”

“From the early days, we felt we weren’t being recognized for the value we brought to the market,” he said. “From almost day one, Dominion Lending Centres Group, including Mortgage Centre Canada and Mortgage Architects and Dominion Lending Centres, were knocking it out of the park. Quarter after quarter were were doing amazing things, but yet we weren’t being recognized for the value we were bringing, especially in the market, under the symbol FCF.”

Mauris added that he and Kayat have personally made sizeable investments in the company this year, proving that they are “100% focused on the future.”

“What it means for us is, we’re going to be purely focusing on Dominion Lending Centres. We think it will have a meaningful impact for our company going forward,” Mauris said.

Pending approval from the TSX, the deal could close by the end of 2020.

And in a second announcement earlier this week, DLC Group announced a franchise agreement with Premiere Mortgage Centre, which counts more than 180 mortgage professionals throughout its network in Ontario and Atlantic Canada.

“We are incredibly pleased to be working with the Premiere Group,” Mauris said in a release. “They are highly respected industry veterans with some of the top mortgage professionals in Canada.”

DLC, with more than 6,000 agents working under its brand name, last year originated $40 billion in funded mortgage, and is on track to originate nearly $45 billion this year, Mauris said.

Meridian Credit Union became the latest mortgage provider to unveil a new interest-only mortgage product.

Meridian, which is the largest credit union in Ontario and second-largest in Canada, positioned its new Hybrid Mortgage as a solution for well-qualified borrowers to increase their buying power.

One of the key benefits of an interest-only mortgage is its ability to lower your monthly payments (since you’re only paying the interest portion) and makes it easier to qualify, even though the mortgage is restricted to those putting down at least 20%.

One of the key benefits of an interest-only mortgage is its ability to lower your monthly payments (since you’re only paying the interest portion) and makes it easier to qualify, even though the mortgage is restricted to those putting down at least 20%.

“Even with a 20% down payment, purchase options for first-time home buyers can be restricted with conventional mortgages, especially for young professionals and recent graduates who may be starting their careers and already have other financial obligations like student loans,” David Moore, Chief Marketing Officer and Senior Vice President Retail Banking, Meridian, said in a release. “Meridian’s Hybrid Mortgage is a creative solution for members who are just starting out on the path of home ownership, so they don’t need to put their dreams for the future on hold.”

And unlike banks and other lenders that qualify borrowers at the mortgage stress test of 4.79%, Meridian qualifies borrowers by ensuring they can afford the monthly minimum payment.

Meridian’s Hybrid Mortgage consists of a variable-rate portion (currently 3.83%) and a 5-year fixed portion (3.92%). Borrowers can only use the interest-only option on up to 60% of their home’s value. Given its non-competitive rates, the Hybrid Mortgage is meant to be a short-term solution, with the intention that most homeowners would transition to a standard mortgage product “as their financial capacity deepens, Meridian notes.