Reasons Why Your Mortgage Application Might Be Denied:

1. Too Much Debt or Too Many Credit Applications: Already having so much debt when applying for a Mortgage can make your lender believe that you are not capable of paying your rates & are not financially stable enough to afford to buy a home right now.

The optimal solution for this would be to pay off as much debt as you can before trying to apply once again. It will also help if your credit applications are minimized as well.

2. Your Credit Score Or History: Your credit score is an important factor that impacts your application.

Make sure to improve your Credit Score to be able to get your mortgage application approved.

3. Your Down Payment: Your deposit may have been too small & your rates calculation didn’t go as planned.

4. You Can’t Afford It: Your lender may have determined that the mortgage you applied for was out of reach for you. This means that the affordability calculations were not made correctly prior to the application.

Want To Discuss More? Send me an email: beataw@dominionlending.ca

EASY: We’ll meet you at a convenient time or place, we can even meet virtually! We take the time to understand your personal situation.

STRESS FREE: We will do the research and compare this with the 100’s of loan products available from dozen of lenders. We’ll present you with some options that provide the best outcome for your circumstances.

QUICK: We can get things moving fast. Once the preferred loan is selected, we do the work of lodging and walk you through the approval and settlement process.

AFTER CARE: We are available any time for queries if circumstances change, and we’ll touch base with you over time, to ensure you still have the right loan for your current situation.

Want To Discuss More? Send me an email: beataw@dominionlending.ca

Ready to take the leap from renter to homeowner? Buying a home is an exciting time, but many potential homebuyers are hesitant due to common misconceptions.

We debunk these common homebuying myths:

Myth #1: Your credit must be perfect to buy a home: Don’t worry; a lower credit score does not automatically disqualify you from getting a loan. Many factors are taken into account, such as your income, debts, assets, and employment history.

Myth #2: You need a certain amount of money in your savings: Generally, it’s a good idea to have a decent amount of money stored away in your savings to help with a down payment, closing costs, and to have available in case of an emergency. However, there is no set amount you need in your savings account to apply.

Myth #3: It is less expensive to rent: Renting and buying both have their benefits and, depending on your situation, one might be a better option for you than the other.

Buying offers the possibility of lower monthly payments and your monthly principal and interest payments will stay the same for the life of a fixed-rate mortgage. In addition, owning a home allows you to build equity, which is wealth you can use to reach your financial goals!

Myth #4: A 30-year loan is the best option: Although many first-time homebuyers elect for a 30-year mortgage, it’s not the only option worth considering. A 15- or 20-year home loan provides a great way for you to spend less money on interest. You just want to make sure this option works well for your budget. A shorter loan term does mean higher monthly payments, but your interest will be lower.

Myth #5: A 20 percent down payment is mandatory: Generally, the more money you put down on a home the better off you will be in the end. While 20 percent is considered the ideal amount – as you will have less to pay back and you will not be spending as much on interest over the life of the loan.

Homeownership is a long-term investment, so the sooner you buy, the larger the potential reward will be later. Invest in your own home today and start enjoying the benefits.

– Your monthly payment goes toward your homeownership.

– You will have an asset that builds equity over time

– You can create the space you want instead of conforming to a landlord

– The expenses in owning a home, like mortgage interest is generally tax-deductible

– Take advantage of programs with low down payment options

– Generate passive income by owning and renting out other properties while living in one of them

Homeownership is the right answer!

Reach out today to see how much you can qualify for.

How Long Does It Take to Get Preapproved For A Mortgage?

No matter if you get preapproved through us, a national bank or a local firm, the steps to getting preapproved are simple.

First, you’ll need to submit a mortgage application. Typically, the lender will then run a check on your credit history and ask you a series of questions about your financial standing and the home you want to buy.

They’ll check your income and assets and analyze your most recent bank statements. Lenders want to ensure that you can pay back the mortgage loan, so they’ll look for any financial red flags like outstanding credit card debt or unpaid medical bills.

After completing the approval process, you’ll receive a letter. If you applied with us, you’ll be in contact with a banker to get a Verified Approval Letter. To be “verified,” you must submit additional documents like tax returns and pay stubs along with the application.

Once you choose a mortgage lender to work with, the preapproval process can take as little as a day to several days.

Top 10 Things to Avoid Before Applying for a Mortgage:

As a homebuyer, you don’t want anything to jeopardise your chances of closing on the home you’ve selected. Making any of the following mistakes could reduce the amount of financing you qualify for, result in a higher interest rate on your mortgage or cause a lender to reject your mortgage application.

Racking up Debt

Forgetting to Check Your Credit

Falling Behind on Bills

Maxing out Credit Cards

Closing a Credit Card Account

Switching Jobs

Marrying Someone With Bad Credit

Co-Signing on a Loan

Making a Major Purchase

Making Big Deposits

Want further info? Message me or Send an email to: beataw@dominionlending.ca

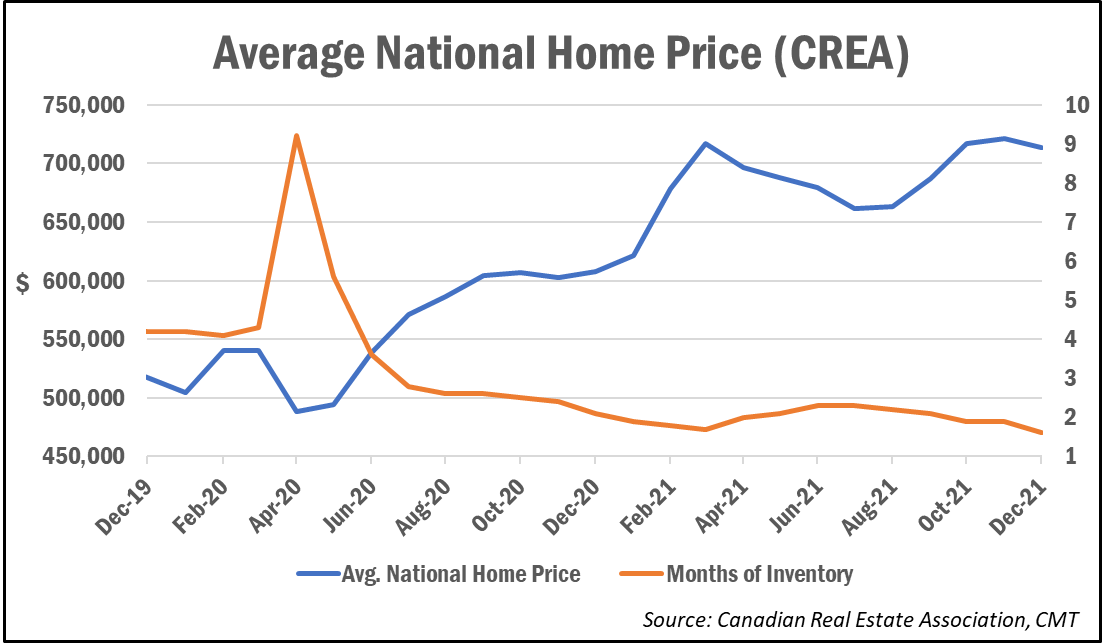

The Canadian Real Estate Association’s House Price Index was up 26% year-over-year as of December, the fastest pace on record.

Analysts say the ongoing price increases are being driven by falling inventory levels and increased demand as buyers try to make their purchases ahead of expected interest rate hikes from the Bank of Canada.

The number of months of inventory fell to a fresh record low of 1.6 months, well below the longer-term average of five months.

The average selling price in December was $713,500, up 17.7% year-over-year on an unadjusted basis, according to the CREA’s latest monthly report. Home sales ticked up in the month, rising 0.2% to 54,366. On an annual basis, home sales totalled 666,995, setting a new record and surpassing the previous high set in 2020 by more than 20%.

“With the housing supply issues facing the country having only gotten worse to start 2022, take any decline in sales early in the year with a grain of salt because the demand hasn’t gone away, there just won’t be much to buy until a little later in this spring,” said CREA chair Cliff Stevenson. “But when those listings eventually start to show up, the spring market this year will almost certainly be another headline grabber.”

Removing the high-priced markets of the Greater Toronto and Vancouver areas, the average price stands at $563,500.

Cross-Country Roundup of Home Prices

In just the past three months, average prices have risen by $125,600 in the Greater Toronto Area, $44,100 in the Greater Vancouver Area, $18,100 in Greater Montreal and $21,600 in Ottawa.

Here’s a look atsome more regional and local housing market results for December:

Ontario: $922,735 (+22.8%)

Quebec: $473,032 (+17.9)

B.C.: $1,031,067 (+22.5%)

Alberta: $420,842 (+7.4%)

Barrie & District: $836,200 (+38.8%)

Greater Toronto Area: $1,208,000 (+31.1%)

Victoria: $902,700 (+23.6%)

Halifax-Dartmouth: $490,127 (+22.2%)

Greater Montreal Area: $517,800 (+21.3%)

Greater Vancouver Area: $1,230,200 (+17.3%)

Ottawa: $661,500 (+16.1%)

Winnipeg: $319,600 (+11.7%)

Calgary: $451,200 (+9.7%)

St. John’s: $292,000 (+9.3%)

Edmonton: $336,600 (+4.1%)

Price pressures could persist throughout the year

As has been the case for several months already, future demand is being pulled forward as buyers try to make their purchases ahead of looming interest rate hikes.

“With interest-rate pull-forward behaviour keeping demand so strong, and supply struggling to keep up, it’s little wonder why prices are continuing their relentless upward march,” noted TD economist Rishi Sondhi. “However, while prices will likely increase this year, higher interest rates should slow the rate of increase. Notably, investor activity is climbing and these buyers are likely more sensitive to higher rates.”

Robert Kavcic, senior economist with BMO Economics, said interest rates have been left too low for too long, which has now resulted in the market becoming “unhinged.”

“Very early last year, BMO Economics warned that policy (starting on the monetary side) needed to tighten in order to prevent the market from becoming dislodged from underlying fundamentals…Now, it appears that 2021 was the year the market became unhinged,” he wrote. “Expectations and investor appetite took over Canadian housing in 2021. We know it, and policymakers now know it too. Look for 100 bps of tightening by the Bank of Canada this year to help clean out some of the froth.”

Even without the extra short-term demand, observers say a chronic shortage of housing supply will continue to keep upward pressure on prices until policymakers get serious about addressing the issue.

“There are currently fewer properties listed for sale in Canada than at any point on record. So, unfortunately, the housing affordability problem facing the country is likely to get worse before it gets better,” said CREA’s chief economist Shaun Cathcart.

“Policymakers are starting to say the right things, but now they have to act to change this course we’re on,” he continued. “An aggressive national push to build more homes is what will address the issue, but it will probably have to be a greater amount of building than anything we’ve ever undertaken. A touch over the status quo won’t cut it.”

The Latest in Mortgage News: CMHC to Review Investment Property Down Payments

It’s no secret that the federal government is eyeing reforms to investment properties in an effort to help reel in runaway house prices.

In a mandate letter sent from the Prime Minister in December, Housing Minister Ahmed Hussen was specifically directed to “review the down payment requirements for investment properties” and develop policies to “curb excessive profits” in that housing segment.

In 2021, over a quarter of all home purchases were made by buyers who already own a home—investors in many cases—according to data from Teranet.

“…our government is looking at every tool at our disposal to tackle these challenges head on,” the Ministry of Housing and Diversity and Inclusion and Canada Mortgage and Housing Corporation (CMHC) told the Financial Post in a statement. “By developing policies to curb excessive profits in investment properties, protecting small independent landlords and Canadian families, and reviewing the down payment requirements for investment properties, we are targeting the issues the market is facing from multiple angles.”

The government has not yet released details on potential changes to investment property down payment rules that are being considered, nor has it provided a timeline for any announcements.

Currently, non-owner-occupied rental properties in Canada with up to four units require a down payment of at least 20% by most lenders.

Mortgage expert Rob McLister told the Financial Post on Wednesday that a five percentage-point-increase to the minimum down payment would likely slow investment purchases “incrementally,” while implementing a 35% minimum down payment would “substantially slow” such purchases.

He added that regulators could also introduce restrictions on the use of borrowed money, such as home equity lines of credit, to fund down payments.

(Updated)

Jason Ellis Appointed CEO of First National

After serving in various roles at First National for nearly 18 years, Jason Ellis has been named the company’s new Chief Executive Officer effective today.

Ellis, who first joined the company in 2004, served as Chief Operating Officer since 2018 and in 2019 added the title of President.

Outgoing CEO Stephen Smith, who served in the role since First National went public in 2006, will continue to provide strategic advice and guidance to management in a newly created role of Executive Chairman.

Smith founded First National in 1988 with Moray Tawse, growing the company to one of Canada’s largest non-bank originators and underwriters of mortgages with $121 billion in mortgages under administration.

“Jason is uniquely qualified to lead First National as my natural successor,” Smith said in a statement. “Passing the baton to Jason is something that I am pleased to do as I know he will take First National to the next level of achievement for the benefit of our employees, customers, partners and shareholders.”

B.C. Saw Record Sales in 2021

More than 124,800 residential units traded hands in British Columbia in 2021, according to final 2021 figures released from the B.C. Real Estate Association (BCREA).

That’s a 33% increase from 2020. Meanwhile, the average MLS residential price in the province was $927,877, a nearly 19% jump from the year before. In three of B.C.’s largest markets, the average price of a home is now over $1 million.

“Last year was a record year for BC homes sales with seven market areas setting new highs,” BCREA Chief Economist Brendon Ogmundson said in a release. “Listings activity could not keep up with demand throughout the year. As a result, we start 2022 with the lowest level of active listings on record.”

Total active listings are currently at a record low of just 12,179 units, down over 41% from 2020.